In our previous blogs ‘A Shot in the Dark’ and ‘Living in the Light’ we unpacked the journey Sarah has gone on. In the last instalment on Sarah, we look into the choices, actions and changes she has made.

Taking control of your finances will give you more freedom than you ever had. Saying no to yourself seems counterintuitive to the definition of freedom but when we take control of our finances saying no to some short-lived spoils will lead to long term freedom. We do not believe in starving ourselves until retirement or sacrificing everything for later but when we go through the process Sarah has gone through, we can see that with a few adjustments we can find true contentment.

A plan that requires foregoing everything you enjoy will fail at some point in the future. We need to enjoy every day that we have but we need to do it wisely.

Learn from the past, enjoy the present and plan for the future.

What can boats teach us about life?

Gaining momentum and changing direction is really challenging. Like many things in life including finances starting a new habit or changing an old one is often the most challenging part of the process.

Using a boat as a metaphor, we know that movement and direction are important to our financial freedom. If you have paddled or rowed in a boat, you know that the first few strokes appear to almost achieve nothing when going from a standstill or changing direction.

In order to change direction or start moving, we need to take action and put in some effort to guide the boat in the new direction. If you have paddled or rowed before you will also know that if you get momentum and start gliding you require less effort to steer and maintain speed. This is similar to finances that if you take the time to work on your habits and direct your plan correctly in the beginning in the future you likely only need minor adjustments.

Sarah understands this and is committed to implementing her plan.

How Does the Plan Come Together?

Over the past few weeks, we have been looking at Money Management and using Sarah as an example. Although we have only had two meetings with Sarah, this process has not been easy. She has had to think, reflect and challenge herself.

With Sarah’s goals now committed to paper, we could draw a map for her to follow. This plan provides an overview and a snapshot of what things could look like in the future.

At this point we should understand a few concepts:

- Monthly expense versus spending habits – What can we change versus what is essential

- Divide and conquer savings method – Breaking down our goals into bite-sized steps

- Compound interest – we need to earn it not pay it

This was the first time that Sarah looked at her expenses in detail. Seeing some of the obvious ways to save money and some of the easy changes she could make to improve really excited her. Not every change is hard and often sometimes just being aware of the mistakes we make is enough to make us change our behaviour.

For Sarah, we gave her the following guidance. We looked at her short-term risks and her medium-long term goals and determined there are a few crucial changes needed to protect her plan. We suggested several expense changes and a few savings changes.

Short Term Risks

if we haven’t put a financial foundation in place, we jeopardise our long-term planning. For example, our car breaking down, being unable to work due to injury or a costly appliance breaking can easily derail our long-term plans. Sarah is including the following in her foundation:

Medical Aid

With the cost of private health care in South Africa, we simply cannot afford to ignore this. Sarah needed a basic hospital plan with some gap cover. There are many different plans and structures and everyone should seek advice for their own needs. There is no need to spend more than you need. We can help evaluate all the options and give you a comprehensive comparison.

Risk Insurance

It is really important to speak to an independent financial planner when looking at life cover, disability and critical illness as these are need-based items in your plan depending on dependents, debt and other sources of income. Independent Financial Advisors are able to compare all the products and at Growmatter our main focus is not commission, but rather your specific need

Sarah has no dependents and very little debt so for now she only needs income protection and a small amount of critical illness cover.

Income protection pays an income should you be unable to work due to sickness or injury. We are dependent on our income and not earning one for even two or three months can ruin any long-term plan we have.

Savings

Sarah implemented the following Savings goals:

An Emergency Fund

We encourage building an emergency fund of 3-6 months expenses. This is crucial in any long-term plan because if something like your fridge breaks and you don’t have the money for a new one it will derail any future plans you may have.

She had a lump sum sitting in a bank account earning interest. We moved that lump sum into a unit trust and started a debit order where it can grow more than the banks rate. This is her first line of defence if something happens.

Paying Off Her Car

Along with the emergency fund this is her next key focus point. She is going to increase her monthly repayment. If she sticks to her goal, she will pay off her car several months earlier. Saving interest and putting her in a position to start saving for her overseas holiday.

Overseas Holiday

She would like to do an overseas traveling holiday through several European countries. We have agreed to revisit this in a year when we review her progress. She plans on paying off her car, saving for retirement and putting an emergency fund in place this is already going to be hard work.

Retirement

It is important to plan for retirement. Statistically only 1 in every 10 South Africans are on track to a full retirement, with the rest of us either retire on way less income or running out a few years into retirement.

- Although some people might have Retirement funds with their work, this often is not enough. It’s important to start as soon as possible and get into the habit of saving. The rule of thumb is contributing 15% of income if you start early enough.

Sarah is part of a pension fund scheme at work which is great because she has made a start but the contributions are not enough. She is needing to start an additional RA. Sarah was lucky to speak to an independent planner because there is a very big difference in retirement products and some have very high fees and horrible restrictions. These products support large upfront commissions in return for tying clients in for a longer time.

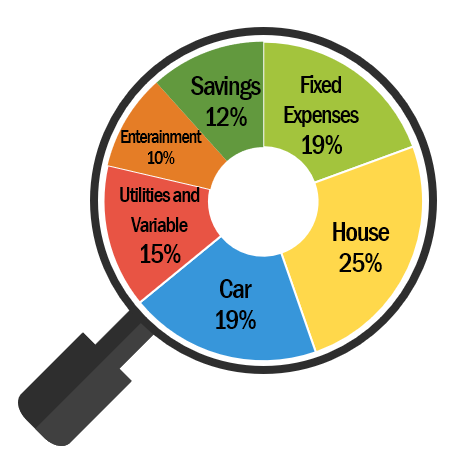

Sarah’s Final Money Management Picture

Through holistic planning and taking all of her goals and needs into consideration we were able to draw up a plan that will reshape her thinking, redefine her future and produce growth that matters.

a BIG disclaimer...

Everybody’s Money Management Plan will look different. This is the adjustments Sarah wanted to make. Your income, savings and needs will be different.

Sarah’s fixed expenses now include Medical aid, Insurance and Donations. Her Groceries and Utilities have been combined. This budget for some is not sustainable but in Sarah’s words, “I am sure I will cope. I live alone and between parents, friends and my entertainment budget I will make it work.”

If you need any financial planning help or guidance contact us. We can review your existing situation and help you save money, improve benefits and ensure you achieve growth that matters.

Live Trust Grow Matter